Why FDI fails: inside Beyond Borders

Published 21 August 2023

Cover image courtesy of ClaudeAI

We now know that the safety of our position in any country depends not alone on our compliance with laws or contracts, or on the rate or amount of our payments to the government, but on whether our whole relationship at any given moment is accepted by the government and public opinion as fair. If it is not so accepted, it will be changed.

So reads an internal Standard Oil (New Jersey, now Exxon) memo from the 1950s, after their concessions in Mexico were nationalised.

Today, embedding investment in a sustainable and positive relationship with citizens is, if anything, even more important.

We’re delighted to be launching a new Reputation Impact consulting service, in partnership with Hanbury Strategy, to support businesses building and managing their reputation in international markets.

Our joint paper Beyond Borders presents research we’ve conducted in the US, UK, Argentina and Nigeria on public attitudes to foreign direct investment (FDI) generally, and energy investment specifically. It identifies five forces in international public opinion shaping the prospects for overseas investment. It also provides practical advice to businesses (informed by robust analysis of local opinion and our combined expertise helping major corporations to date) seeking to understand public opinion, develop and communicate reputation, and ultimately mobilise support behind strategic investments.

In simple terms, our research reinforces the point that Standard Oil articulated 70 years ago: that in any country, a firm’s reputation matters fundamentally in generating public support, which is essential in securing their position with governments and regulators.

But every country is different. Attitudes vary, drivers of reputation vary, and intensity of feeling across issues varies. Understanding these dynamics of local opinion is crucial for any organisation, particularly those operating in politically sensitive sectors.

In this post, we delve deeper into the data to draw out three generalisable themes that emerge from the multi-country research.

Politics matters

Figure 1: Coefficient plot of the effect of being a centre-right voter on warmth towards foreign investment

Warmth towards foreign investment was measured on a 100-point scale. The reference voter/baseline is a centre-left party voter. A coefficient of -10 indicates that a centre-right voter, on average, has a warmth score (towards foreign investment) that is 10 points lower than a comparable centre-left voter. Models control for age, gender, education, and region. Whiskers show 95% confidence intervals.

Political dividing lines are a crucial part of understanding attitudes towards business and foreign direct investment. But our research shows that these dividing lines are not stable or consistent across markets. Instead, public attitudes and electoral coalitions are constantly shifting in response to cues from political actors.

As the report sets out, one such realignment is taking place in the US and UK in respect of FDI and free trade more widely. In the US, centre-right voters now hold outright protectionist views while in the UK the traditional relationship between support for the Conservatives and support for business has broken down. That shift is not observable in other countries, like Argentina, as Figure 1 shows, where centre-right voters hold warmer views towards foreign investment than same-country centre-left voters. Where once centre-right voters could be relied on to be broadly supportive of trade, investment and economic openness, that is no longer necessarily true.

In the face of a wide array of global crises (including the war in Ukraine, global inflation pressures, and the energy transition), as well as slower-moving but no less significant challenges like ageing populations across the Western world and rising levels of migration, we should expect these kind of political realignments to become the norm.

Prosperity matters

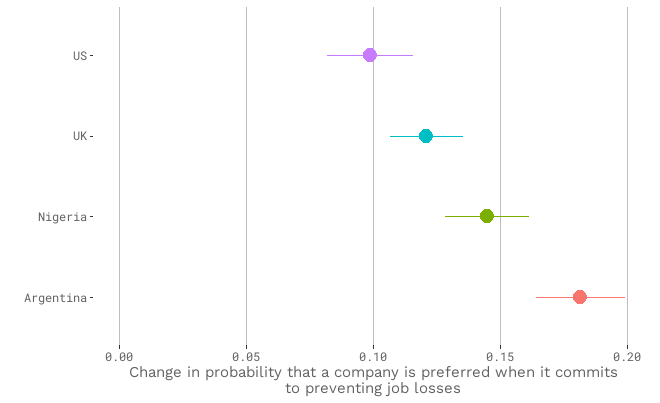

Figure 2: Coefficient (AMCE) plot of the effect of ‘committing to prevent job losses’ on the likelihood of a company being preferred by a respondent

General attitudes to FDI vary between the two relatively prosperous countries (UK and US) and the two relatively lower-income countries (Nigeria and Argentina) in our research: respondents in the latter two countries are considerably more optimistic about the impact of foreign investment than are respondents in the former. (An examination of the income crossbreaks across the 4 countries shows, too, that those with incomes above the respective national medians are more optimistic than those on lower incomes.)

In our conjoint experiment, we asked people to choose between two hypothetical firms with randomly varying features. By aggregating their responses, we can then estimate the isolated effect of individual features on company favourability. One of these features was whether or not a company credibly commits to providing jobs to local communities. We find that this commitment had a much greater effect on company favourability in Nigeria and Argentina than in the US and the UK (see Figure 2). This suggests there’s a hierarchy of concerns ranging from the essential (employment, or the reliable availability of energy, for example) to the desirable (environmental commitments, or the sustainable production of energy) and that businesses will need to tailor their approach to maximise support for investment in different markets.

Finally, an interesting angle on generating support for energy investment within more prosperous countries: incentives. The report points out the damaging gap between the energy investments people believe are necessary and their willingness (or unwillingness) to see such infrastructure being built in their own area, a problem that is particularly acute in the UK.

But as Figure 3 shows, financial incentives do work: taking the building of a nuclear power plant as our example, 17% of people who don’t support the building of a nuclear power plant in their local area become supportive when asked “To what extent would you support plans to build the following in your local area if it meant that you would receive much cheaper energy as a result?”

NIMBYism poses a challenge in other areas too - notably housebuilding - and this research suggests that testing financial and other incentives to unlock local support may be worthwhile.

Figure 3: Alluvial chart of the effect on support for development of nuclear power (in the respondent’s local area) of adding a financial incentive

History and culture matter

Figure 4: Coefficient plot of country-level effects on warmth towards foreign investment (0-100 scale. UK = 0, baseline)

Finally, we find clear evidence that public opinion is downstream of history and culture. Any investor looking to crack these cultural codes needs to begin with a deep examination of public attitudes.

Even after controlling for all other variables (demography, political beliefs, economic situation) there are discernible country-level effects. Figure 4 below plots differences in attitudes to FDI (“Where 0 is ‘extremely negatively’ and 100 is ‘extremely positively’, from 0 to 100, how do you feel about a foreign company buying a business in your country?”). Taking UK attitudes as our baseline, and - again - after controlling for all other variables, we see considerable variation in attitudes that are explained only by the country in which the respondent lives.

Our recent experience working in an eastern European country neatly highlights this challenge: through a large-sample foundational poll with open-text questions asking respondents to describe things they love about their country, we found that the population cherishes the country’s reputation as an agricultural power. Proposed investments to extract natural resources from within an agriculture-heavy part of the country therefore faced opposition not only from members of the proximate community, but also more widely from those who shared this deeper pride in the country’s reputation as the breadbasket of the region.

Techniques to get reliable insight into public opinion on complex topics

Finally, a note on why research design and methodology really matters when carrying out this kind of research. One challenge with polling on esoteric subjects like FDI is that the average person doesn’t walk around with a fully-formed opinion on such things. The inherent risk of only asking discrete choice questions (“On balance, do you prefer…”, or “To what extent do you agree or disagree that [statement]”) is magnified: not only does the usual “It depends” risk apply, we also can’t assume that respondents themselves have a more nuanced view than the question itself presents.

Figure 5: Bar chart of the effect of the different attributes on company favourability (or technically, the probability that a company is preferred compared to a company without that attribute)

We routinely try to understand public opinion on complex subjects, and have found conjoint analysis a particularly effective technique. To isolate the underlying drivers of reputation - the things ordinary people might care about in relation to theoretical investments by notional businesses - we showed each respondent several pairs of “profiles” of a foreign investor. Each profile contained randomly generated characteristics (e.g. “Is French”, “Has been complimented on its sustainability efforts”, “Has committed to providing 1,000 new jobs in the area of investment”), and we asked each respondent to pick their preferred investor of the pair.

That allows us to conclude with real confidence that whilst nationality matters, the single biggest driver of potential public support for a firm is having a reputation for treating its partners and employees well.

Conjoint coefficients (the bars in Figure 5) show the effect of moving from the baseline feature to the feature listed on the left. For example, the coefficient for “Chinese” shows that if we change investor nationality from “Australian” (baseline) to “Chinese”, we find a 14% drop in the likelihood of respondents selecting that company as their preferred investor.

The size of the gap between the coefficients relating to how a company is reported to treat its employees underlines how essential a positive employer reputation is for achieving public support: having a reputation for treating employees and partners well translates into an 18% improvement in support versus a counterfactual where a company has the opposite reputation.

Read the full Beyond Borders report here